Employment Ownership Trusts (EOTs) and why they are becoming increasingly popular

Article

29 June, 2021

EOTs were originally introduced by the Government in September 2014, in an attempt to encourage more shareholders to set up a corporate structure similar to the John Lewis model, by offering significant tax breaks. However, it took until the 2020/2021 tax year for the utilisation of EOTs to substantially spike - this is likely due to the impact of the COVID-19 pandemic and the anticipated rise in UK Capital Gains Tax.

For more information on what an EOT is, please see our recent article on EOTs.

This article will explain how a sale of shares to an EOT works, consider the advantages / disadvantages of selling to an EOT and explore why many shareholders are now choosing this sale method, over the usual sale to a third-party investor.

How does it work?

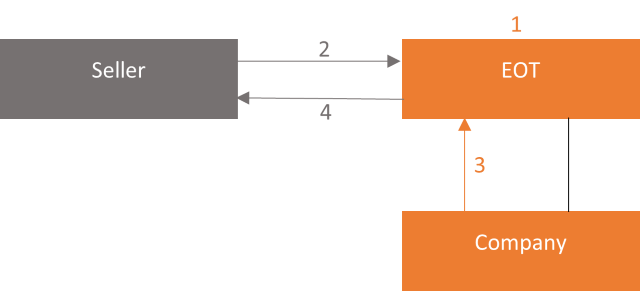

The sale of a company to an EOT works as follows:

- A qualifying EOT will be established with a corporate body as the trustee of the EOT (the Trustee Company).

- The shareholders sell their shares to the Trustee Company under a share purchase agreement. The shareholders and the Trustee Company will jointly engage a share valuation expert to value the company: the Trustee Company will use this value as the basis for determining the purchase price. On the sale of the shares, the purchase price will create a debt owed by the Trustee Company to the shareholders which will be left outstanding.

- The company will continue to generate trading profits each year and it will use these profits to make contributions to the EOT.

- The EOT will use these contributions to repay the outstanding purchase price that it owes to the shareholders.

What are the advantages?

The advantages for the selling shareholders are:

- It allows employees to indirectly buy the company from its shareholders without them having to use their own funds - thereby creating an immediate purchaser and addressing succession issues

- Shareholders can sell their shares for full market value (an independent valuation will be required)

- No capital gains, income or inheritance tax liabilities should arise on the disposal of a controlling interest in a company to an EOT (or on the subsequent receipt of the purchase price by the former shareholders)

- Not all shareholders are required to sell their shares to the EOT

- The directors can remain in situ post-disposal and can continue to receive market-competitive remuneration packages

- The EOT is generally seen as a "friendlier purchaser" which means the sale process may be quicker, with potentially lower fees.

Also, companies controlled by EOTs are able to pay tax-free cash bonuses to their employees of up to £3,600 per employee per year.

What are the disadvantages?

An important point to be aware of when a company is sold to an EOT is that the purchase price is fixed at the point of sale. Therefore, should the value of the company increase post-disposal, the selling shareholders would not be entitled to any additional consideration.

Due to the way in which these transactions are generally financed, it is important that the trading company remains profitable and cash-generative post-disposal. This is because, as the original shareholders' deferred consideration is generally financed via the post-tax profits of the trading company, should the trading company become loss making then it may be unable to make payments to the EOT which in turn would mean that the trustee of an EOT may unable to pay some, or all, of the deferred consideration.

Case Study

ADT Workplace Limited (ADT), a Manchester-based interior design and delivery specialist, has recently become fully employee-owned, by transferring 100% of the business into an EOT.

The founders of ADT, including the Board Director, John Clemeston, consider that some of the key drivers for the change to a EOT structure were:

- to build a solid platform for growth

- to improve job stability

- to reward the employees that have grown the business to be the success it is today

- retain the culture and empower everyone to drive the business forward

- and leave a legacy for future succession planning

Discussions were held with the Employee Ownership Association (EOA) and the benefits of placing the business into an EOT were explored - ADT soon realised this was the perfect fit for the business and now was the right time to make this move.

Is an EOT right for you?

You should consider a sale of shares to an EOT if:

- You don't feel a trade sale or management buyout is feasible or the best solution

- You wish to sell your shares, but are struggling to find a third-party investor in the current climate.

- You are looking to take advantage of the generous tax breaks, in light of recent proposals to increase CGT

We strongly recommend that you seek tax/financial advice before proceeding with any company restructuring or sale of shares.

For more information contact David Filmer in our Corporate department via email or phone on 0333 207 1132. Alternatively send any question through to Forbes Solicitors via our online Contact Form.

Learn more about our Corporate department here

Contact Us

Get in touch to see how our experts could help you.

Contacting Us

Monday to Friday:

09:00 to 17:00

Saturday and Sunday:

Closed